A small announcement from eBay last week. Most people probably didn’t notice it, given the news around Q3 earnings, Skype, and 100 other stories that people were tracking.

Here is the AuctionBytes article:

eBay Moves to Longer Lasting BIN Auctions

Actually, eBay began testing this back in July, but just recently expanded it to quite a few more categories. Here is the original note from Sohil Gilani, the Product Manager who has spent a lot of time over the past two years studying and implementing this change:

Hi everyone, I’m Sohil Gilani with our Buyer Experience team. Over the years, we’ve routinely been asked why the Buy It Now option disappears from a listing when the first bid is placed. Our reason has been concern that it would create a confusing experience for a buyer, who could place a bid on an item, but then have someone Buy It Now (BIN) out from under them before the end of the auction. That said, we’ve done some extensive research that suggests keeping the BIN option available on a listing longer will increase the chance that a buyer wins the item and that it will close at a higher price for the seller. As a result, we’re looking at ways to change how BIN works that balance both buyer and seller needs.

In case it isn’t clear, let me explain the problem:

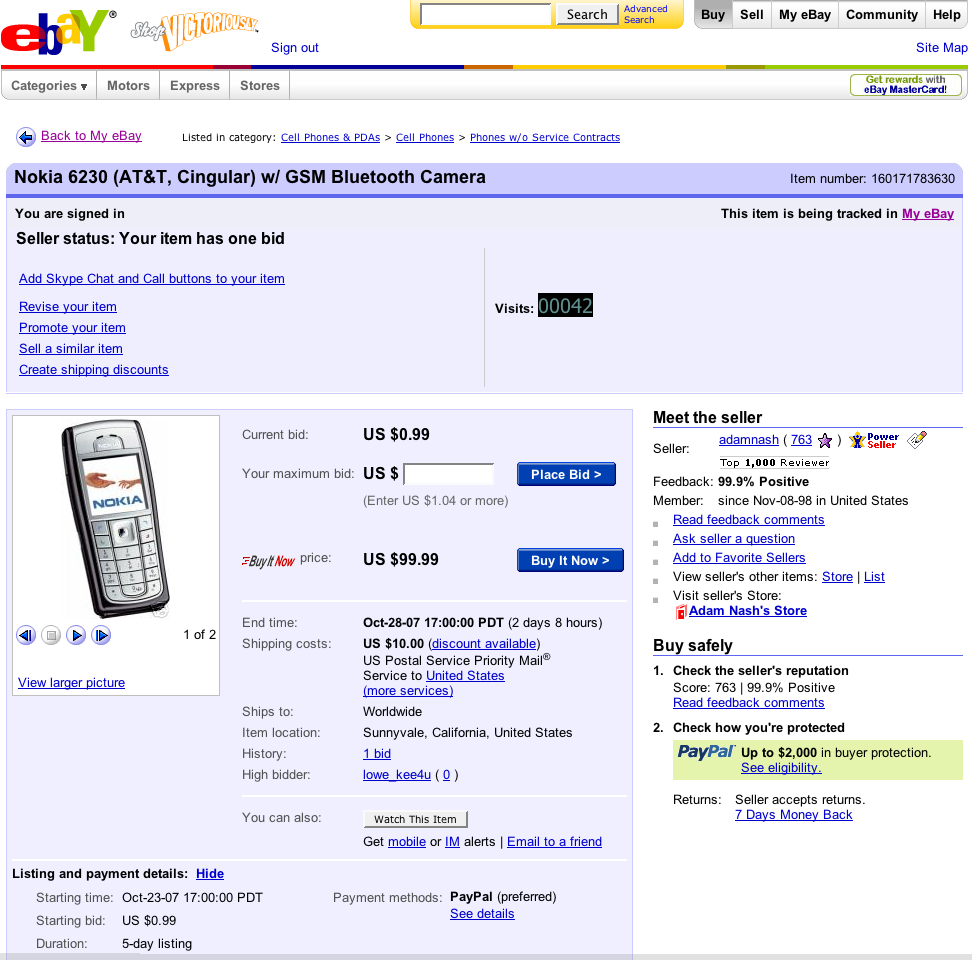

Ever since eBay launched the ability to add a “Buy It Now” button to an auction, it has disappeared as soon as anyone placed a bid. So, for example, if you were auctioning a cell phone with a starting bid of $0.99 and a Buy-It-Now price of $99.99, a single bid of $1.00 would make the Buy-It-Now price disappear.

The idea is that a buyer has the chance to “snap up” the item for a fixed price set by the seller, or place a bid to try to win it at auction. Usually, the motivation to place a bid is the belief that the bidder will get it for a lower price.

The problem is, once the Buy It Now button disappears, every future potential buyer is deprived of two things:

- The ability to immediately buy the item, without waiting for the auction to end

- The ability to see what the seller thought a fair “fixed price” was for the item

Many people, for a very long time, have asked why eBay makes the BIN button disappear after one bid. Usually, they focus on issue (1). After all, the need to wait for an auction to end is a major disincentive for a potential buyer. eBay is likely losing quite a few buyers to the fact that useful BIN buttons are disappearing. Sellers are also losing the ability to close a sale quickly, for a fair price that they have assigned. Even worse, sellers actually pay eBay a fee to place that BIN button there in the first place.

The problem lies with issue (2). As a former employee, I can’t reveal the actual number, but you would be shocked at how many auctions actually close at a price higher than the original Buy It Now price. This happens for a couple reasons. First, sellers may not be very efficient at setting their own fixed prices – auctions are likely much better at fairly pricing the item. Second, the original bidder who “knocks out” the BIN button is not likely the one who bids above that price. Every future bidder has now lost that information, and as a result, is free to bid whatever they think is fair. Apparently, in a large minority of cases, bidders end up with a price that is higher than the seller expected.

So, eBay has a dilemma:

- If they keep the disappearing BIN button, they are likely losing sales AND velocity (the time it takes to close a sale). They are also encouraging sellers to use a higher starting price (to avoid losing the BIN quickly), use reserve prices (to keep the BIN), or to not use BIN at all (which is a fee-generating feature) – all bad things that hurt the likelihood of a sale.

- If they make the BIN sticky, aka “Persistent BIN”, they might actually decapitate the final selling price on millions of auctions. That would hurt both eBay sellers and eBay itself, since both make money based on the final sales price.

The solution that eBay is testing finally allows eBay to gain some empirical data in real situations on how to best control the way the BIN price disappears.

- Do you let the BIN button stay until a fixed dollar amount?

- Do you let the BIN button stay until a fixed percentage of the final price?

- Are the results different in different categories? For different starting prices?

Well, all I can tell you is that, as an eBay seller, I was tickled pink to see this on my latest cell phone auction this week:

As you can see, I start all my auctions with a starting price of $0.99. Normally, I lose that BIN button very quickly. But in this case, the BIN button stayed, even after a bid of $0.99. In fact, the button stayed until the bidding reached $50.00, giving buyers ample opportunity to buy my phone for fixed price. The difference? Literally 6 days of BIN button goodness were added, since my auction didn’t clear that price until the 7th day.

(Wow, that sounds like a biblical reference. It was evening and it was morning, and the BIN button worked for 6 days and 6 nights, but on the 7th day, the BIN button rested…”)

Anyway, I’m glad to see eBay continuing to push its understanding of one of its most popular formats. And a big congratulations to Sohil for seeing this effort through to live-to-site. Count me as a big fan.

BTW If you are wondering why I bother buying the BIN feature on my auctions, even though it disappears so quickly, it’s a fair question. In my selling experience, adding the BIN button not only increases the chances of my auction selling quickly, I also tend to set it for a higher-than-average price based on my research. The way I see it, a buyer who wants it right now tends to be willing to pay a bit more for the privilege. If not, they can always bid.